The Product

Simple, Powerful, Automated.

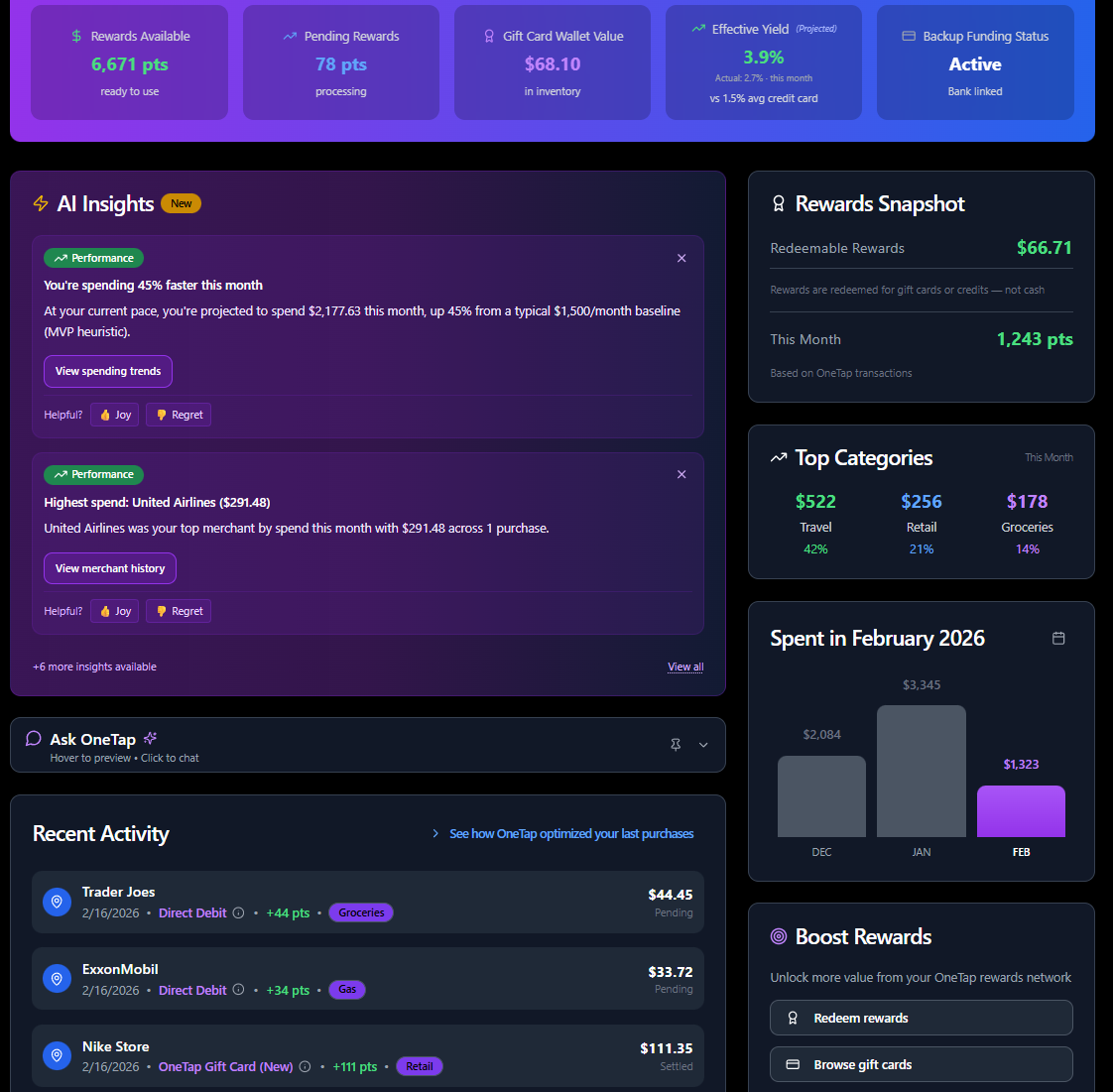

And we don’t stop at routing—OneTap becomes your financial OS with intelligent insights.

OneTap is designed to be effortless. In three simple steps, users can transform their spending and maximize their rewards.

1

Link Your Funding Source

Connect your existing bank account or debit card. OneTap acts as your intelligent buffer.

2

Spend Anywhere

Use the OneTap virtual or physical card.

3

The AI Orchestrator

Our "OneTap Brain" instantly identifies the merchant. If a high-yield rail (Gift Card) exists, it executes an instant purchase. If not, it pushes a standard debit charge.

My Wallet

3 Cards Linked

Chase Debit Card

•••• 1234

Wells Fargo

•••• 5678

Bank of America

•••• 9012

+ Link Another Account